PRNs in the age of EPR: What does this mean for the market?

Matthew Austin, Senior Market Analyst at Ecosurety, revisits how the UK’s packaging recycling obligations have evolved in light of the latest PRN market data.

In an article last year, I explored how the UK’s packaging recycling obligation might evolve under the first year of Extended Producer Responsibility (EPR), and what this could mean for the PRN (Packaging Recovering Note) markets.

It was a response to the then draft statutory instrument – which is now law – and raised concerns about the new recycling targets.

I cautioned that the 2025 recycling obligation could be lower than in recent years, and potentially lead to oversupplied markets and reduced revenue for recyclers.

The article garnered attention from colleagues across the industry. Some shared similar concerns while others challenged the approach taken, but all agreed on the importance of ensuring that we have a functioning PRN system to support investment in UK recycling.

So, where are we now, one year on and halfway through the first year of EPR?

Demand: A mixed bag

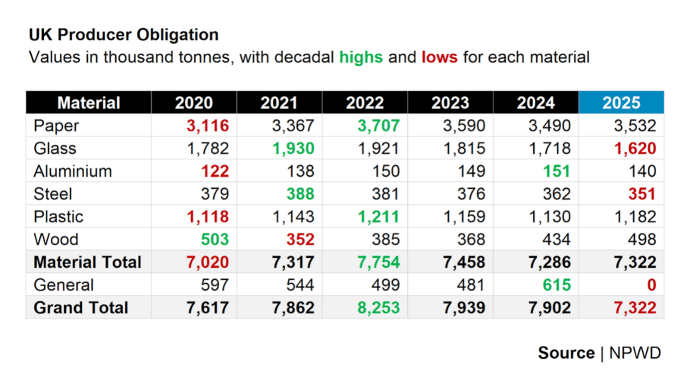

Recycling obligation is the demand side of the PRN system and, under EPR, is calculated from data submitted to the Report Packaging Data (RPD) service. The most recent data snapshot is from 02 June 2025.

The data can be read in two different ways. The initial takeaway is that total obligation looks to be the lowest this decade due to there being no general recycling obligation under EPR. However, the 2025 obligation appears more ‘normal’ if we compare it to the material totals from previous years.

Even so, there is variation at a material-specific level. Both wood and plastic are close to their decadal highs, whereas glass and steel are at their respective lows.

Steel is generally considered a declining packaging material, so this is perhaps to be expected, but the shift in glass is interesting. Is this lower obligation due to the new recycling targets, or is it perhaps a result of rapid material substitution in response to high waste management fees for glass?

To summarise, it’s a bit of a mixed bag. While fewer PRNs are technically needed this year due to the removal of the general recycling obligation, this only really impacts cheaper materials; paper and wood PRNs were typically used to fulfil it.

For other materials, particularly plastic, the obligation is looking relatively high, and markets could be quite tight.

Of course, this could all change as the year progresses and more producers submit data. Indeed, a quick comparison of the public list of large producers shows around 1,250 fewer producers registered for 2025 than in 2024 (where producers reported data under both the EPR and 2007 regulations).

Supply: A slow start

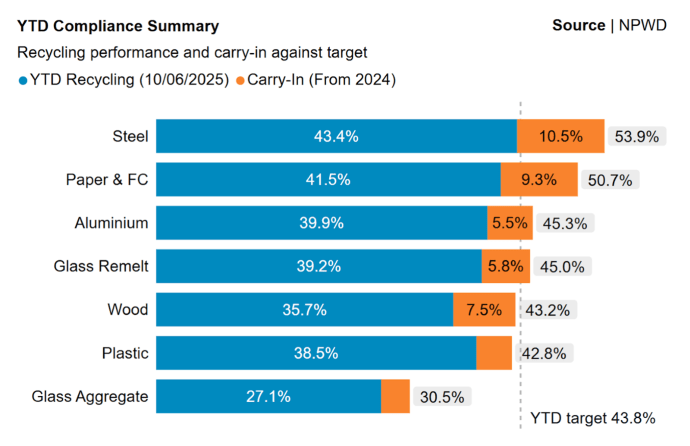

The latest supply data (the number of PRNs generated) was published on 10 June 2025. Set against the newly published obligation – pro-rated for where we are in the year – we can see some obvious areas of concern, even when the carry-in from last year is factored in.

The key takeaway is that no material is currently on track to meet in-year compliance – obligation being met without needing carry-in from the previous compliance year. If we include carry-in, plastic and wood appear to be slightly under where they need to be, with glass aggregate being significantly below target.

By comparison, there had been 204 thousand tonnes more recycling at this point last year, when obligations were generally lower and there was less carry-in. Put another way, demand is slightly higher this year yet year-to-date supply has been relatively weak.

The obvious caveat here is that monthly reporting is not mandatory and, therefore, tends to be understated. However, it is the best we have at this stage of the year.

Reaction: Surprisingly rational?

Regulatory transitions are complicated, and EPR is no exception: a bold, industry-wide paradigm shift with the potential to revolutionise our understanding of packaging flows and apply the polluter pays principle more fairly.

The problem, of course, is that doing something new is hard – and there isn’t always the data to predict outcomes with certainty. However, the early signs are cautiously optimistic.

The Department for Environment, Food & Rural Affairs (Defra) had the almost impossible task of setting recycling targets without knowing how much packaging would be reported under the single point of compliance. To have gotten as close to 2024 obligations under a completely different system is an impressive feat.

While my prediction of a lower overall obligation appears to have been accurate, I overlooked a crucial nuance in my article last year: on a material-specific level, obligations are broadly similar. Thankfully, I was wrong about the market reaction. The PRN system is proving resilient.

The markets appear to be acting rationally and broadly in alignment with the data fundamentals. Prices have adjusted in line with the new obligation levels, and volatility has so far been limited – at least relative to recent standards – which is encouraging.

Looking ahead

A high PRN price supports high-quality recycling, but too high a price can lead to an increase in fraud. Persistently low prices have the opposite effect, discouraging reprocessors from registering altogether.

The ‘sweet spot’ is a price high enough to adequately compensate reprocessors while being low enough for producers to be able to comply with the regulations.

Recycling targets are a key mechanism for calibrating the relationship between supply and demand, and at this point in the year, they appear to have been set at competitive but not unachievable levels.

One could argue that materials such as paper, steel and possibly glass could benefit from minor target increases, but the overall picture is looking broadly positive.

With a new consultation on the horizon, we look forward to working with Defra, the regulators and other industry bodies to help reform and improve the PRN system.

More data and transparency would be welcome, as well as mechanisms to support long-term investment in the UK’s reprocessing infrastructure.

Amid an ever-changing regulatory landscape, it is perhaps reassuring that the PRN system – an ambitious relic from the early days of producer responsibility – continues to operate well into its third decade.

The post PRNs in the age of EPR: What does this mean for the market? appeared first on Circular Online.

You May Also Like

Environment Agency grants permit for Exeter landfill site

Scottish EfW facility treats 1 million tonnes of waste